Rent vs buy

For a $1,500,000 home (20% down, 6.5% mortgage) vs renting at $4,500/mo — assuming 3.5% home appreciation and 7% investment returns — after 5 years renting comes out ahead by about $392k. Renting wins if a similar home rents for under $9,865/mo. Adjust everything below — and see which assumptions actually move the answer.

Methodology#

The comparison follows the standard "invest the difference" approach: the renter invests the buyer's upfront cash (down payment + closing costs) and, each year, the difference between the buyer's total cost of ownership (mortgage payment, property tax, insurance, maintenance) and rent — in whichever direction it runs. The buyer's wealth is home equity net of selling costs; the renter's is the portfolio. Annual compounding; mortgage amortized monthly. Simplifications: no mortgage-interest tax deduction (the post-2017 standard deduction makes it irrelevant for most households), no capital-gains taxes on either side, no PMI or HOA (add them to maintenance if relevant), and constant rates throughout. The point of the sensitivity views is precisely that these second-order terms matter far less than the appreciation-vs-returns spread. Estimates for planning, not financial advice.

FAQ

- Is it better to rent or buy?

- It depends almost entirely on four things: how fast the home appreciates, what your investments would earn instead, how long you stay, and the rent-to-price ratio of your market. Under typical assumptions (3.5% appreciation, 7% investment returns, staying 5 years), renting comes out ahead for a $1,500,000 home vs $4,500/mo rent — but small changes in those inputs flip the answer, which is what the sensitivity charts on this page show.

- What is the most important variable in rent vs buy?

- The spread between home-price appreciation and what your invested money would earn otherwise. A house is a leveraged bet on home prices funded by cash that could compound elsewhere — if stocks outrun your home by a few points a year, renting usually wins; if the home keeps pace (with leverage), buying does. Mortgage rate, rent growth and how long you stay come next; insurance, taxes and closing costs rarely change the verdict.

- How long do I need to stay for buying to make sense?

- Upfront costs (closing, then ~6% selling costs) mean buying starts several tens of thousands behind and catches up over time. Under this page's default assumptions the breakeven is beyond 40 years — but check the "Advantage over time" chart with your own numbers.

More visualizations

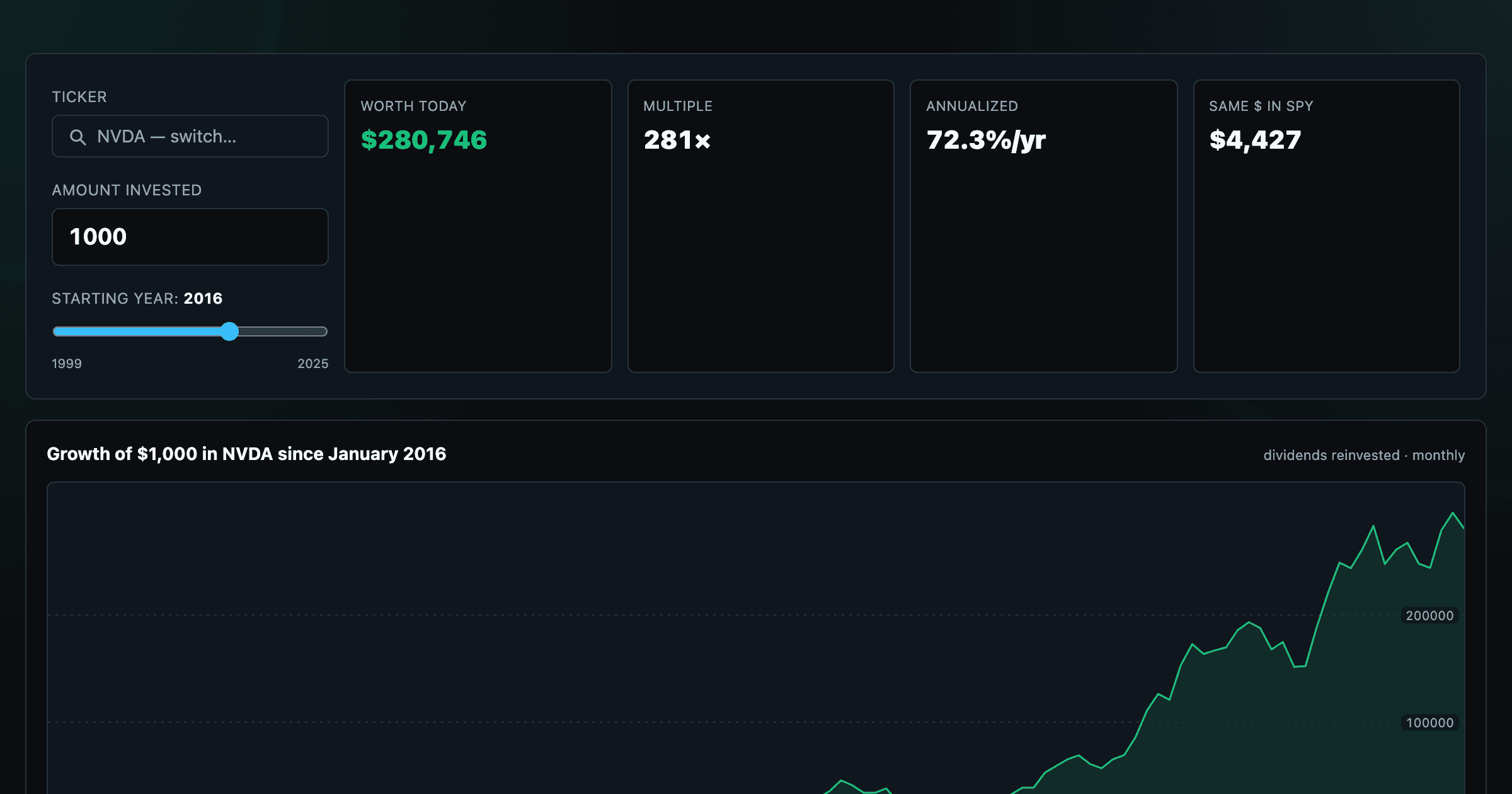

What $1,000 in any stock or ETF would be worth today.

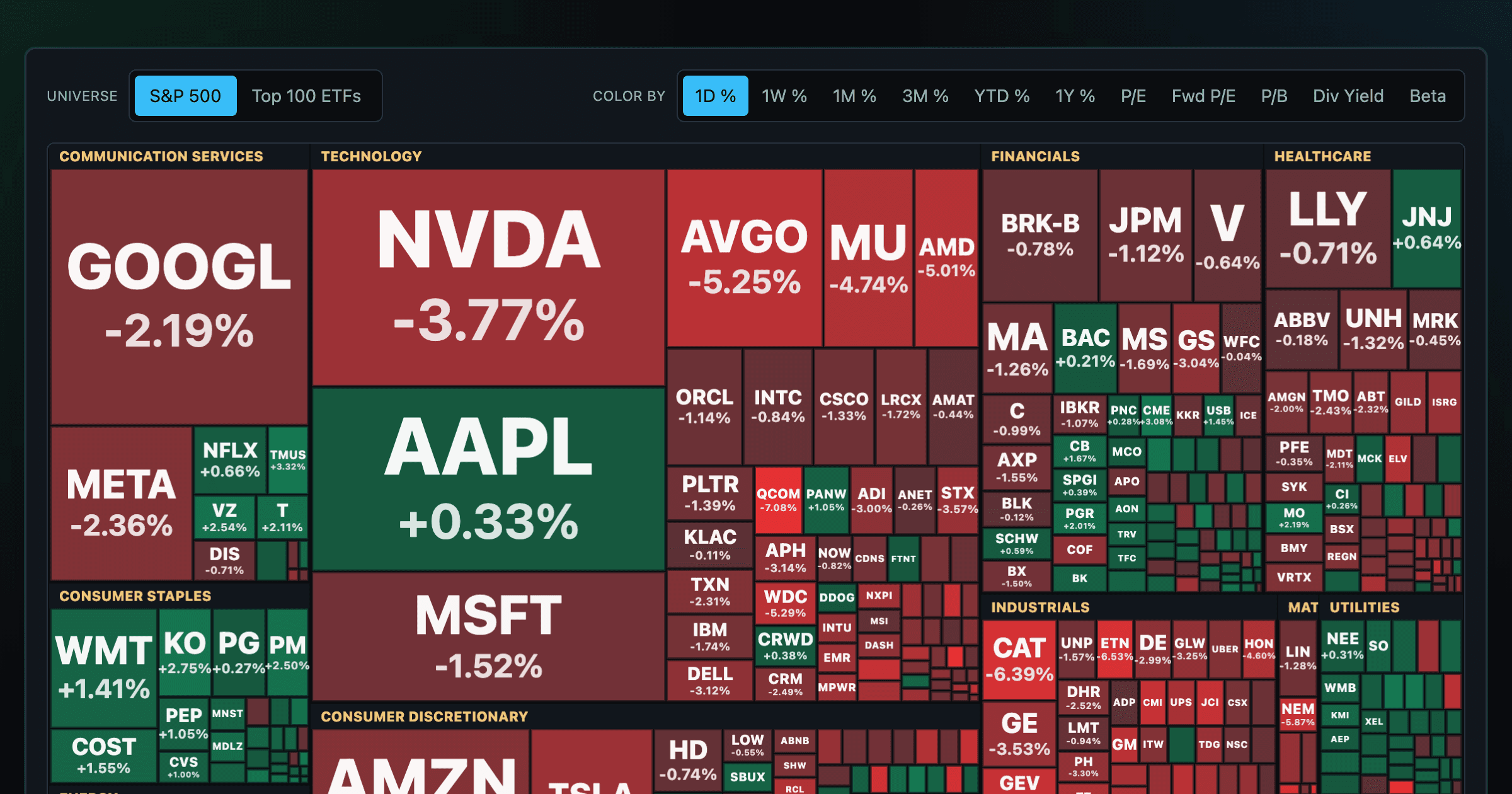

Every S&P 500 company sized by market cap — color by return or valuation.

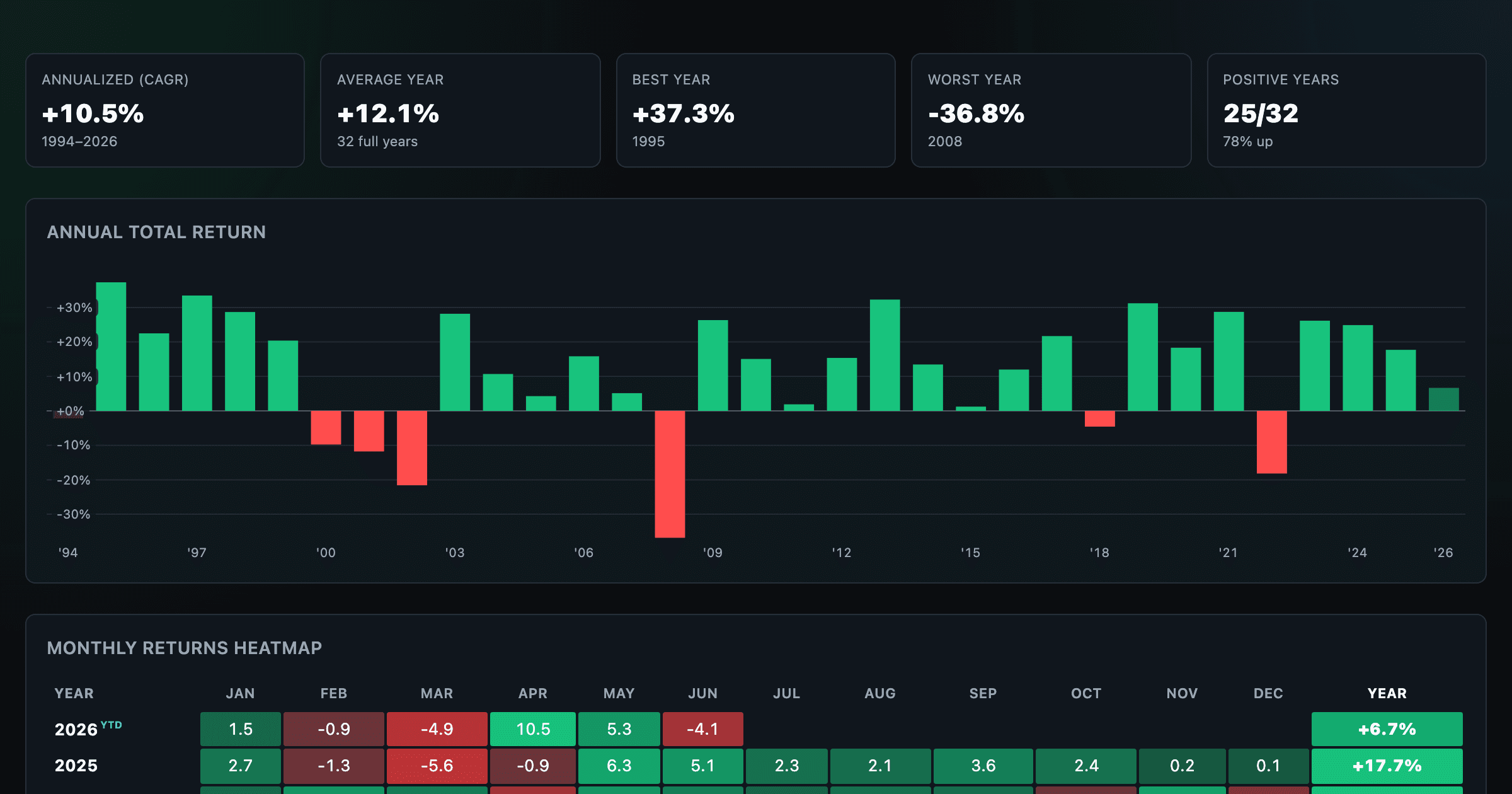

S&P 500 returns by year, month, week and trailing period — total or price return.

Which month is best for stocks? Average return of every calendar month, for any ticker.

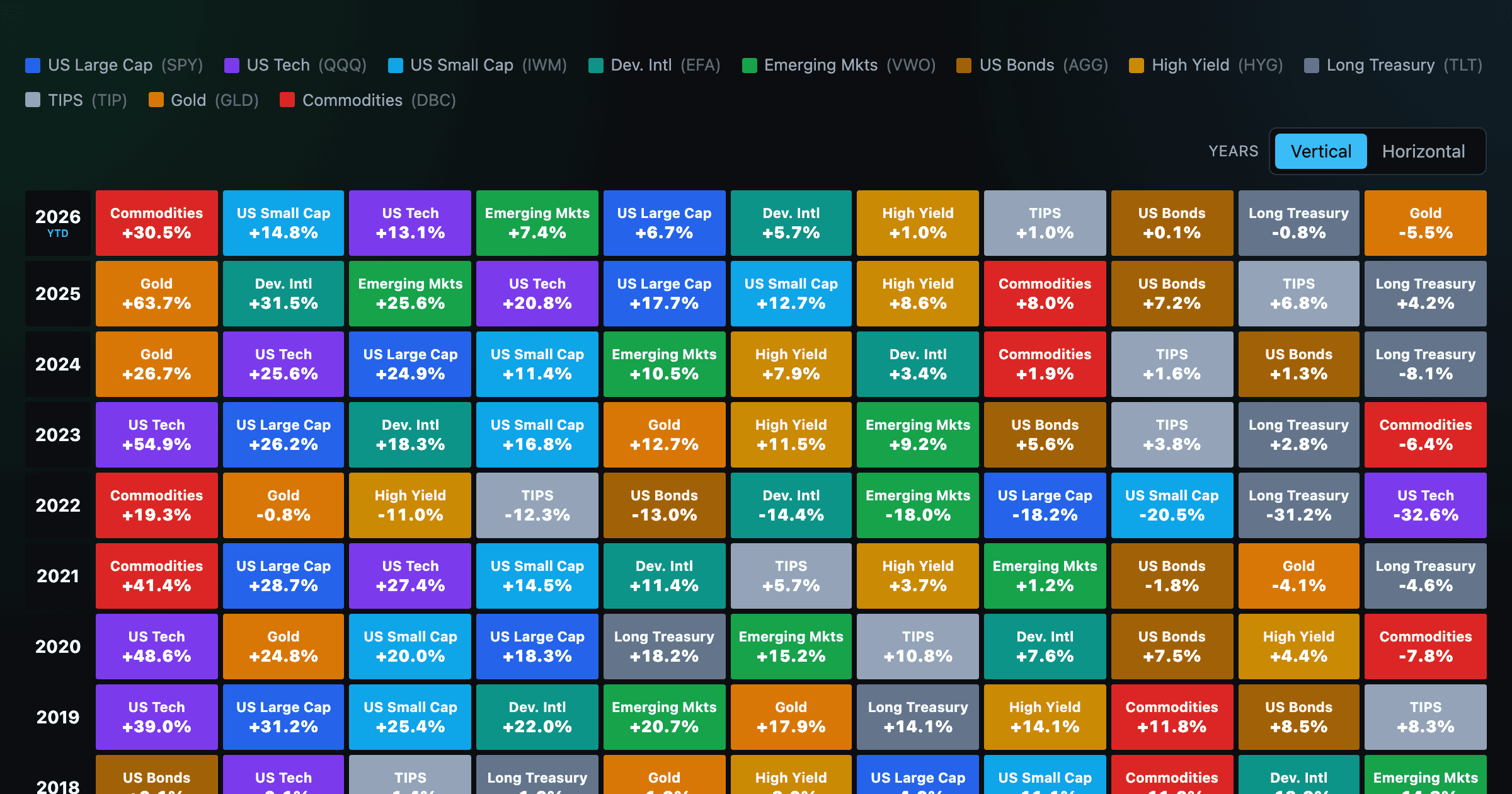

Asset-class returns ranked year by year — the Callan chart / asset allocation quilt.

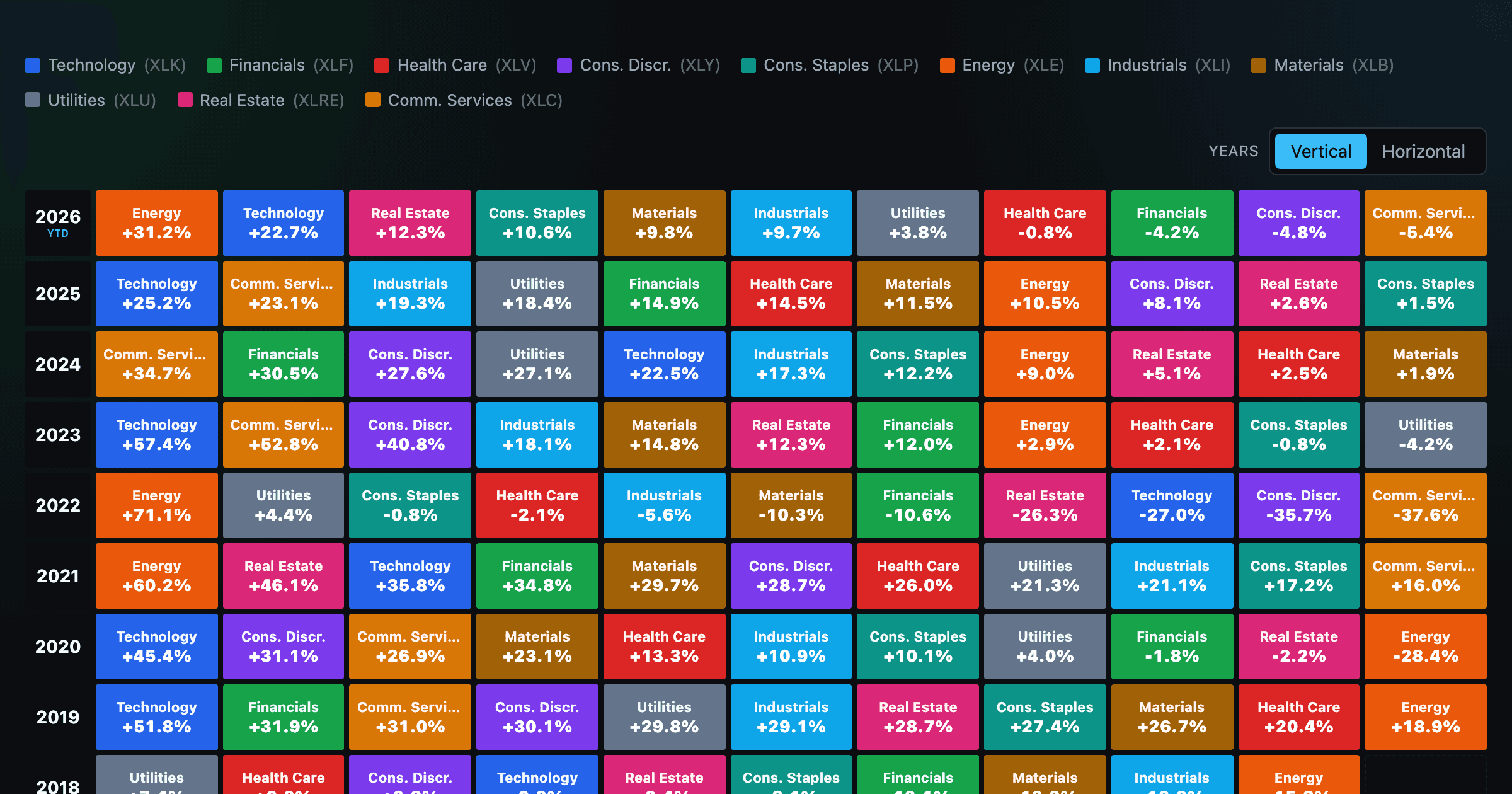

The 11 S&P 500 sectors ranked year by year — a sector quilt chart, back to 1999.

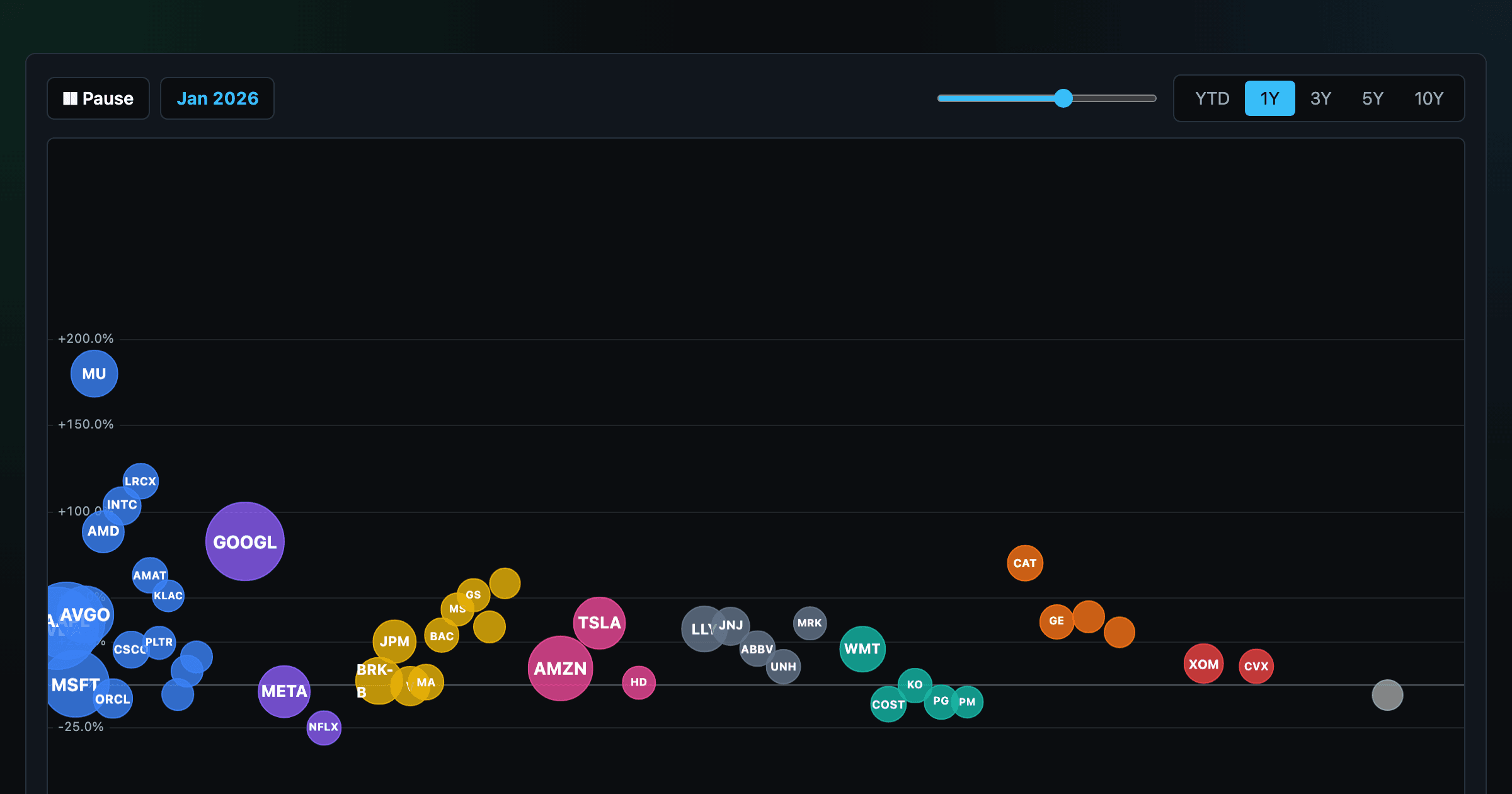

The biggest US companies as animated bubbles, rising and falling with their total return over time.

How recent stock-market debuts have performed since listing — annualized, vs the S&P 500, by IPO vs spin-off.

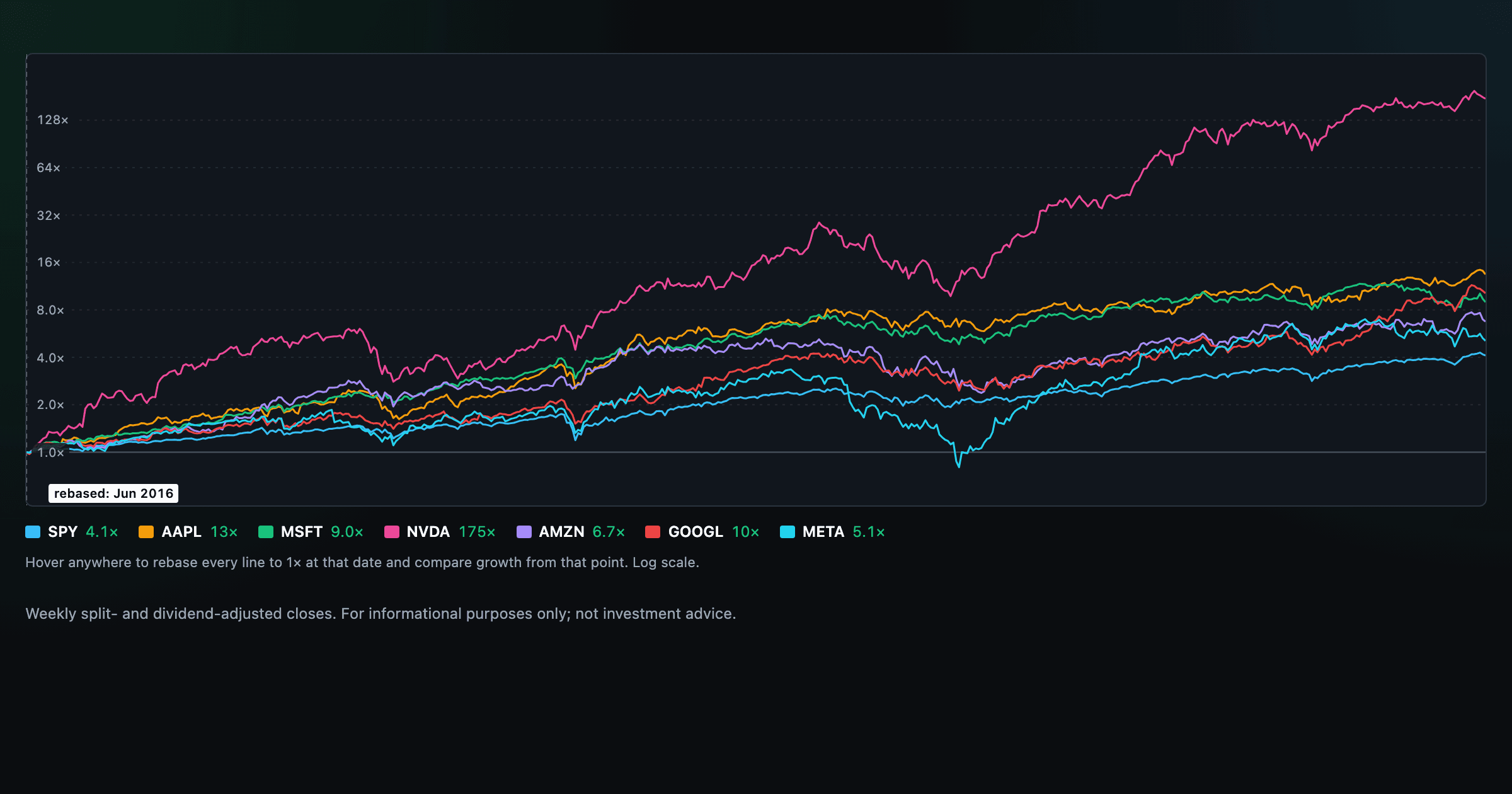

Compare megacaps vs the S&P 500, rebased to 1× at any date you hover.

Where today's S&P 500 return ranks against all history — and the forward returns that followed similar moments.

Is the market expensive? The Shiller CAPE back to 1871 and what valuations have meant for the next decade.

The S&P 500 since 1871 — odds of gain by holding period, real drawdowns, and the growth of $1.

Stocks trading cheapest relative to their own P/E, P/FCF, P/S, or P/B history — with fair-value bands.

Follow a company's revenue through its income statement as a Sankey — costs, taxes, and profit.

Follow a company's cash from net income through operating cash flow into capex, buybacks, and dividends.

Monthly payment, principal vs interest by year, and the balance paydown — with extra-payment savings.

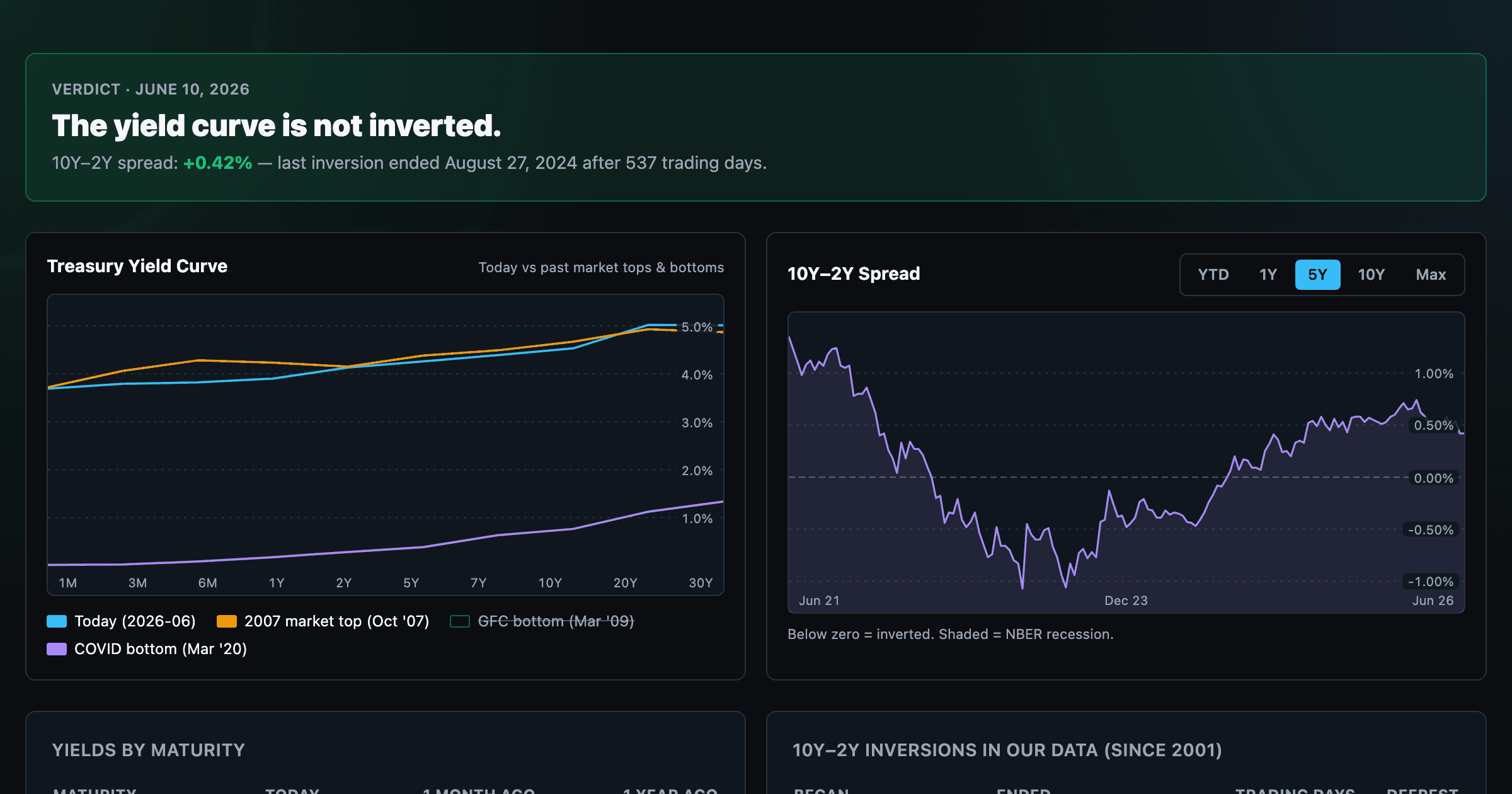

Live term structure, the 10Y–2Y spread, and every inversion episode.